June 10th, 2026

Every time a guest taps, dips, or swipes their card at your restaurant, a fee leaves your account before you ever touch that revenue. Most operators know fees exist, few understand how they’re layered. Understanding the stack is the first step to managing it.

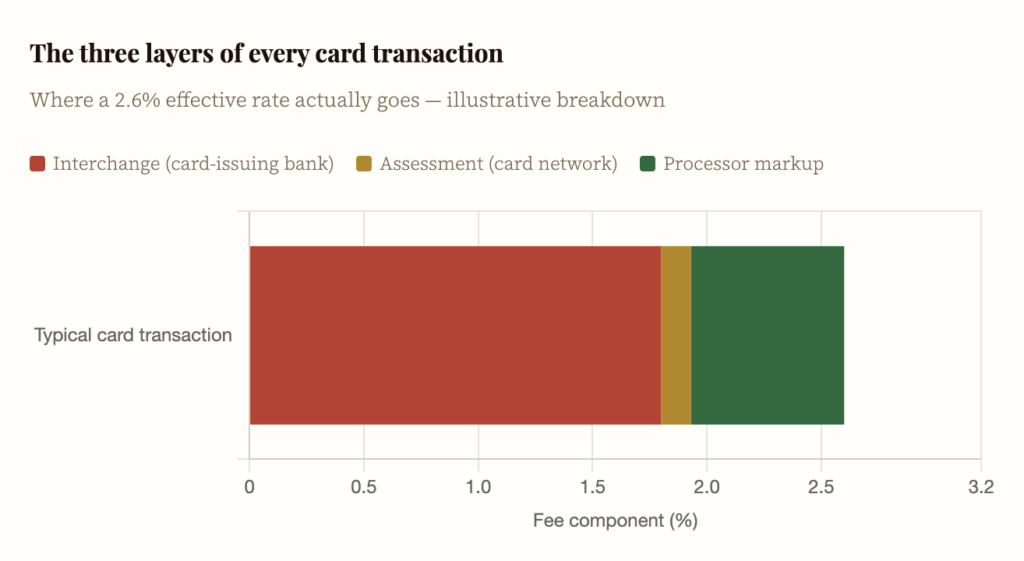

A payment processing fee is not a single charge. It is a bundle of three distinct costs flowing to different parties:

1. Interchange

Interchange is the fee paid to the bank that issued the customer’s card. It is set by Visa, Mastercard, Discover, and Amex and it varies enormously. A basic Visa debit card may cost you 0.05% + $0.22 per transaction. A premium rewards card (“Infinite” or “Signature”) issued by a major bank can run 2.3%+ plus a fixed per-transaction fee. You do not control which card your guests use.

2. Assessment fees

Visa charges 0.13% on every Visa transaction. Mastercard charges 0.1375%–0.1500%. These go directly to the network and are largely non-negotiable. They are small but unavoidable.

3. Processor markup

The processor (Square, Toast, Stripe, Heartland, Shift4, etc.) adds a markup on top of interchange and assessments. This is the only part of the fee you can negotiate. It can be structured as a flat per-transaction add-on, a percentage, or a monthly fixed fee.

Rule of thumb: Interchange represents roughly 70–80% of total processing costs. Assessment fees represent about 10%.

Processors offer your fees in different packaging. The structure determines how predictable your costs are and how much you pay at different volume levels and ticket sizes.

|

Structure

|

How It Works

|

Type

|

Best For

|

|---|---|---|---|

|

Flat-rate

|

One % + per-transaction fee regardless of card type (e.g. 2.6% + $0.10)

|

Flat

|

Low-volume cafés, food trucks, quick-service under $500K/yr

|

|

Interchange-plus

|

Actual interchange cost + fixed markup (e.g. interchange + 0.3% + $0.10)

|

Trasnparent

|

Full-service, fine dining, high-ticket restaurants over $500K/yr

|

|

Tiered / bundled

|

Cards bucketed into "qualified," "mid-qualified," "non-qualified" tiers with different rates

|

Opaque

|

Common in legacy POS bundles, often the worst value; avoid if possible

|

|

Subscription / membership

|

Monthly fee ($50–$100) + true interchange pass-through at near-zero markup

|

Fixed

|

High-volume restaurants processing $2M+ annually

|

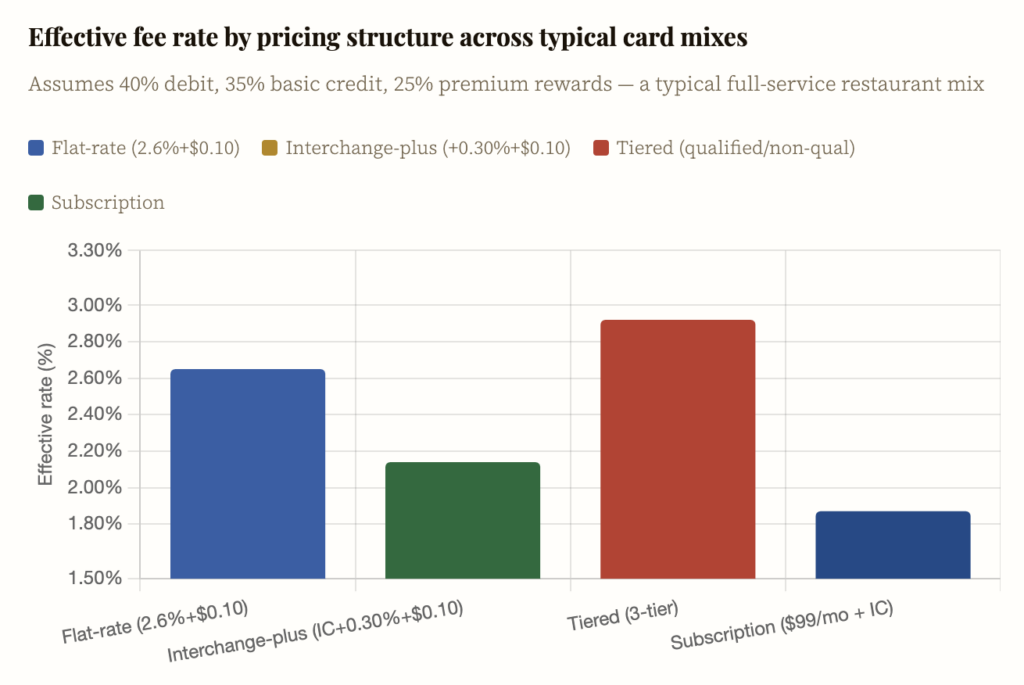

Square’s 2.6% + $0.10 in-person rate is the canonical example. You know exactly what you’ll pay. The problem: you pay the same rate whether your guest uses a basic debit card (whose interchange is 0.05%) or a premium rewards card (whose interchange is 2.3%). On debit transactions, the processor pockets a large spread. Simple accounting can hide expensive costs.

With interchange-plus pricing, your statement shows the actual interchange for every transaction type, then adds a fixed markup. You can see exactly what you’re paying and to whom. At high volumes, this typically saves 0.2%–0.5% versus flat-rate, material on $1M+ in revenue.

Legacy POS companies often default to tiered pricing. Cards are sorted into tiers based on opaque criteria, and “non-qualified” (rewards, corporate, foreign) cards get routed to the highest-rate tier. Restaurants that have switched from tiered to interchange-plus have reported effective rate reductions of 0.4%–0.7%.

Raw percentage fees are abstract. The impact becomes visceral when you map them onto actual restaurant economics. Consider that full-service restaurants typically operate at 3%–9% net profit margins. A 2.5% payment fee is therefore not a rounding error, it can represent a third or more of your total profit.

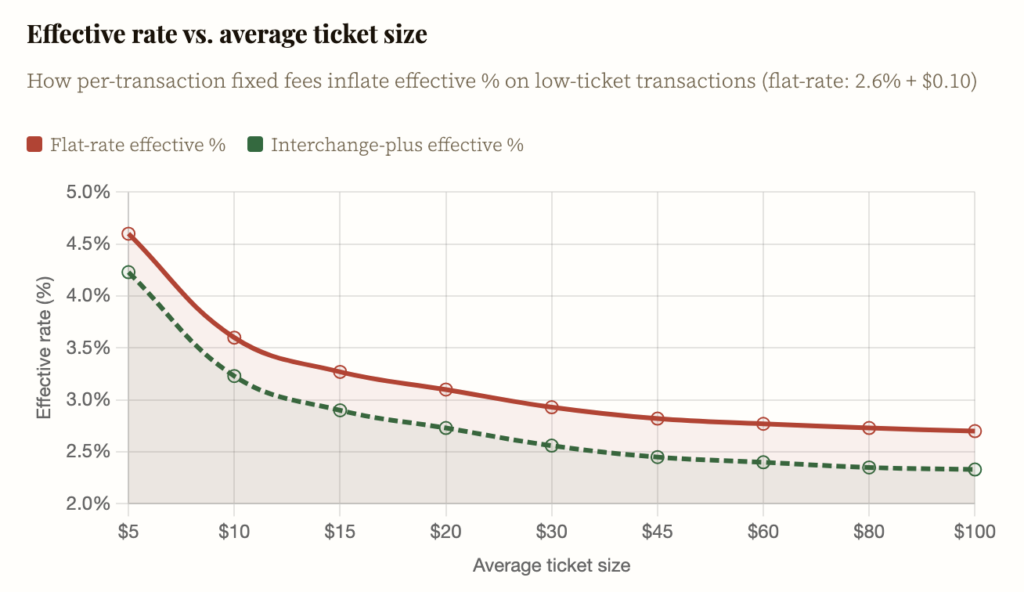

Every fee structure has a per-transaction fixed component (typically $0.05–$0.15). This per-transaction fee hits low-ticket venues disproportionately hard. On a $5 drip coffee, a $0.10 fixed fee represents 2% before the percentage component is even added.

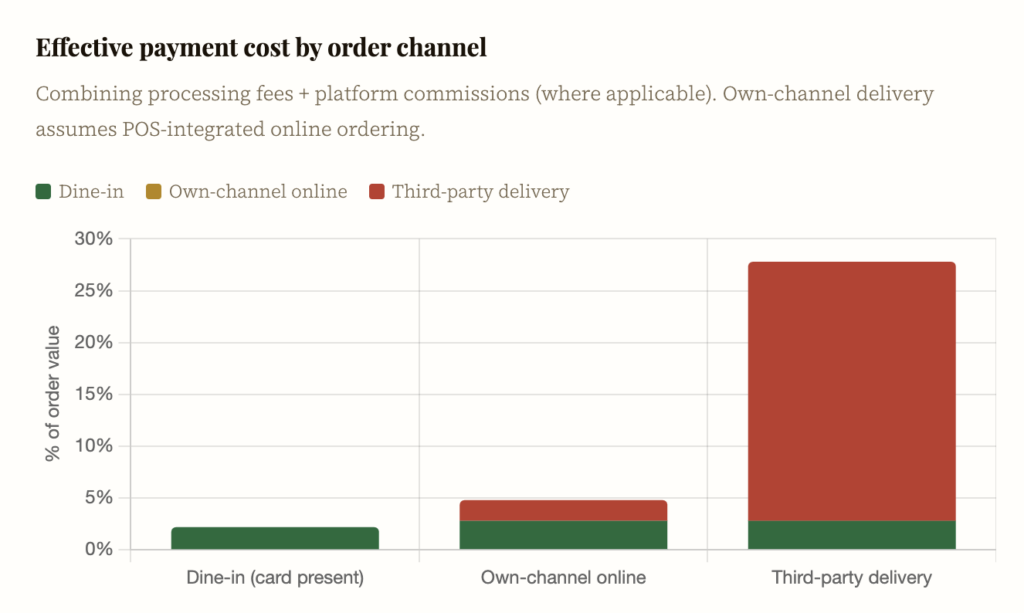

Online orders: whether through your own website, DoorDash, Uber Eats, or Grubhub are classified as card-not-present (CNP) transactions. The card isn’t physically presented, so the risk of fraud is considered higher, and interchange rates increase accordingly. CNP interchange can run 0.4%–0.8% higher than card-present rates.

For restaurants where 30–50% of revenue now flows through delivery channels, this is a structurally higher cost base that didn’t exist a decade ago.

Delivery app double fee trap: Third-party apps like DoorDash charge you a platform commission (15%–30%) and pass through payment processing fees on top. You are effectively paying fees twice. Own-channel ordering (via your website or branded app) eliminates the platform commission entirely.

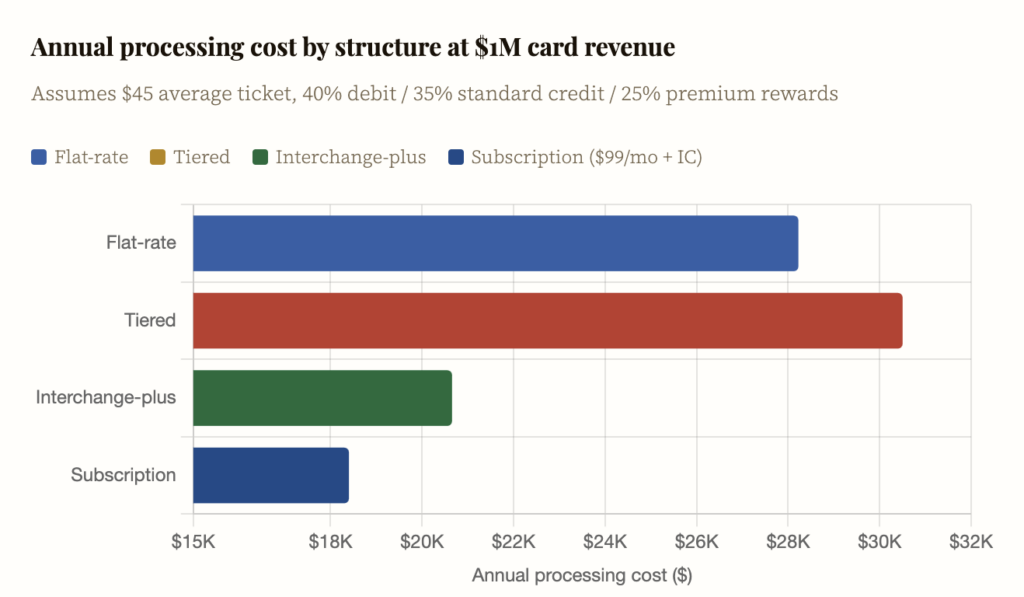

Let’s ground this in concrete dollars. Consider a full-service restaurant doing $1,000,000 in annual card revenue, with an average ticket of $45 and a card mix of 40% debit / 35% standard credit / 25% premium rewards.

Flat-rate calculation:

$1,000,000 × 2.6% = $26,000

+ 22,222 transactions × $0.10 = $2,222

= $28,222 total fees

Interchange-plus (estimated):

Debit ($400K) × 0.62%: $2,480 | Std credit ($350K) × 1.65%: $5,775 | Premium ($250K) × 2.35%: $5,875

Interchange subtotal: $14,130

Assessments (~0.13%): $1,300

Markup (0.30% + $0.10/txn): $3,000 + $2,222 = $5,222

= $20,652 total fees (saving ~$7,570 vs flat-rate)

The exact saving depends heavily on your actual card mix. Restaurants with more corporate and premium-rewards customers see even greater savings switching to interchange-plus because those high-interchange cards are disproportionately cross-subsidised by flat-rate payers.

The advertised rate is only part of the story. Most merchant agreements include a constellation of secondary fees that can add 0.3%–0.8% to your effective rate without appearing in the headline number.

|

Fee

|

Typical Cost

|

What To Wathc For

|

|---|---|---|

|

Monthly minimum fee

|

$25–$50/mo

|

Charged when processing volume doesn't generate minimum fee revenue. Hits seasonal/low-volume spots hard.

|

|

PCI compliance fee

|

$60–$180/yr

|

Some processors charge even when you're already compliant. Others charge non-compliance penalties that dwarf this.

|

|

Chargeback fee

|

$15–$35/dispute

|

Win or lose, you often pay this. Delivery channels have higher chargeback rates.

|

|

Early termination fee

|

$200–$500+

|

Can trap you in a bad contract. Always read the exit clause.

|

|

Gateway fee

|

$10–$25/mo + $0.05/txn

|

Separate from processing charged by the payment gateway for online/CNP order routing.

|

|

Annual/statement fees

|

$50–$150/yr

|

Administrative fees that vary widely. Sometimes negotiable.

|

Monthly statement audit tip: Download your full merchant statement (not the summary). Calculate your “effective rate” as total fees ÷ total card volume. If this number is more than 0.3% above your quoted rate, hidden fees are materially eroding your margins. Ask your processor to itemise every line.

The shift toward off-premise dining has fundamentally changed restaurant fee economics. A restaurant that was 100% dine-in five years ago and is now 40% delivery faces a structurally different fee profile, one that most operators haven’t fully modelled.

The third-party delivery channel is uniquely punishing because the platform commission and the higher CNP processing fee stack on top of each other. On a $25 delivery order through a major aggregator, you might surrender $6.50–$8.50 in combined fees: 26%–34% of the ticket.

Own-channel wins: Investing in direct online ordering (via your own website or a white-label solution) eliminates platform commissions while keeping CNP rates. At even modest volume, the fee savings exceed the cost of the technology within months.

Interchange and assessment fees are set by the card networks, non-negotiable. But processor markup is entirely negotiable, and most operators never attempt it.

The leverage framework is straightforward:

Volume threshold

Processing less than $250K/year gives limited leverage. At $500K–$1M, you can typically reduce markup by 0.1%–0.2%. At $2M+, you have meaningful negotiating power and should consider interchange-plus or subscription pricing.

What to negotiate

Target the processor markup rate, the per-transaction fee, monthly minimums, PCI compliance fees, and early termination terms. Get quotes from three processors even if you intend to stay with your current one. Written competing quotes are the most effective negotiation tool.

Timing

Your contract renewal date is your highest-leverage moment. Many processor contracts auto-renew with a 30–90 day notice window. Calendar this and act proactively rather than reactively.

Payment processing fees are one of the most overlooked cost centres in restaurant operations. They never appear on a food invoice, they’re buried in dense merchant statements, and they compound quietly across tens of thousands of transactions.

The practical takeaways are clear:

In an industry where net margins rarely exceed single digits, every basis point recovered from processing fees flows directly to the bottom line. Treat payment costs with the same rigour you apply to food cost.

In most U.S. states and Canadian provinces, surcharging credit card transactions is permitted, but it comes with strict rules. Visa and Mastercard require visible disclosure, a cap on the surcharge amount (typically 4%), and the surcharge can only apply to credit not debit. Many operators fear customer pushback; the reality is that a well-communicated “credit card fee” or a dual-pricing (“cash discount”) model is increasingly common and accepted, particularly in high-ticket segments. Always check the rules in your specific jurisdiction before implementing.

Yes, significantly. Many POS systems bundle processing at rates you cannot renegotiate, because the hardware and software are subsidised by the processing spread. Open-architecture POS systems (Lightspeed, RPOWER) allow you to bring your own processor. Before choosing a POS, always model the total cost of ownership including processing rates, not just hardware and software subscription costs. A “free” POS with a 2.9% processing rate can cost far more over five years than a paid POS with interchange-plus at 2.1%.